Minneapolis

Background

Minneapolis is the largest city in Minnesota, with a growing population of around 450 000 people. It is the first city in the U.S. to abolish single-family-zoning as part of the Minneapolis 2040 plan which came into force in 2020 and allowed triplexes to be built on most blocks. However, the upzoning story here is far more complicated than in Auckland.

The impact of the single-family zoning abolition has drawn a great deal of media attention and scrutiny. (See, for example here or here) There has been an increase in the number of Triplexes and Quadplexes built, but they remain only a small amount of the total housing supply. It is possible (and perhaps likely), that over time more will be built, as there was an increase in prices for plots upzoned relative to those not upzoned (those just outside the Minneapolis city border) with price increases greatest for plot areas with greater amounts of vacant space and smaller existing dwellings (Kulhmann 2021). This reflects that the market values the ability to build multiple dwellings.

But, the abolition of single-family home zoning was part of the Minneapolis 2040 plan, but it was only one small element of upzoning - some argue that other reforms are more important. Transit corridors were upzoned, and minimum height limits were set in dense areas. (In complete contrast to other zoning systems, Minneapolis actually rejected a development for being too short in 2021 – an 8-storey building had to be re-proposed to 10 stories.) Maximum dwelling occupancy caps were scrapped, and changes to Accessory Dwelling Unit (ADU) rules made it easier to build granny flats and backyard apartments. Mandatory parking minimums were eliminated.

As the plan is very recent, it’s true impacts are as yet unclear because building completions and development require time. Furthermore, the plan was temporarily blocked in June 2022 due to a lawsuit from environmental groups, but was allowed to procced in July until a full legal ruling is made.

The other complication in Minneapolis’s upzoning story is that reforms and housing supply began before the 2040 plan’s implementation - making it difficult to see impacts before and after reforms. Housing supply began to increase around 2012 and has generally trended up (albeit with some fluctuations). Some of this may be attributable to reductions in the minimum ratio of parking spots to new dwellings and some liberalisation of ADUs toward the start of the decade (See the Upzoning Tracker). Indeed, the average parking spots built per dwelling has now dropped by around 40% since 2011, which reflects that the previous level of parking built was inefficient. This has likely made some projects financially viable, as parking is hugely expensive in dense developments. It is also plausible developers began to build new dwellings prior to the 2040 plan’s implantation as they were aware of the city’s pro-density stance.

Parking per dwelling

Supply

Plexes Construction

Supply and Rents

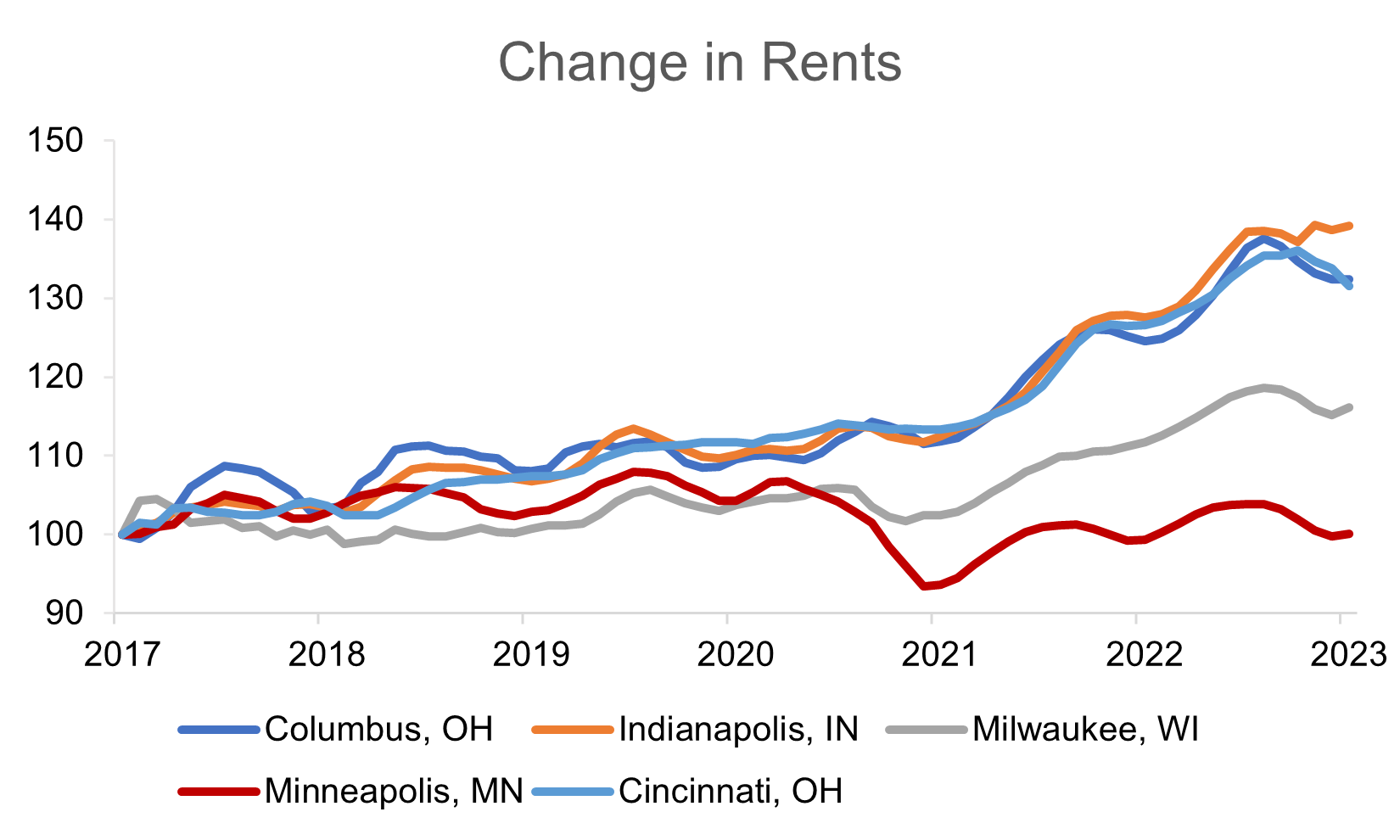

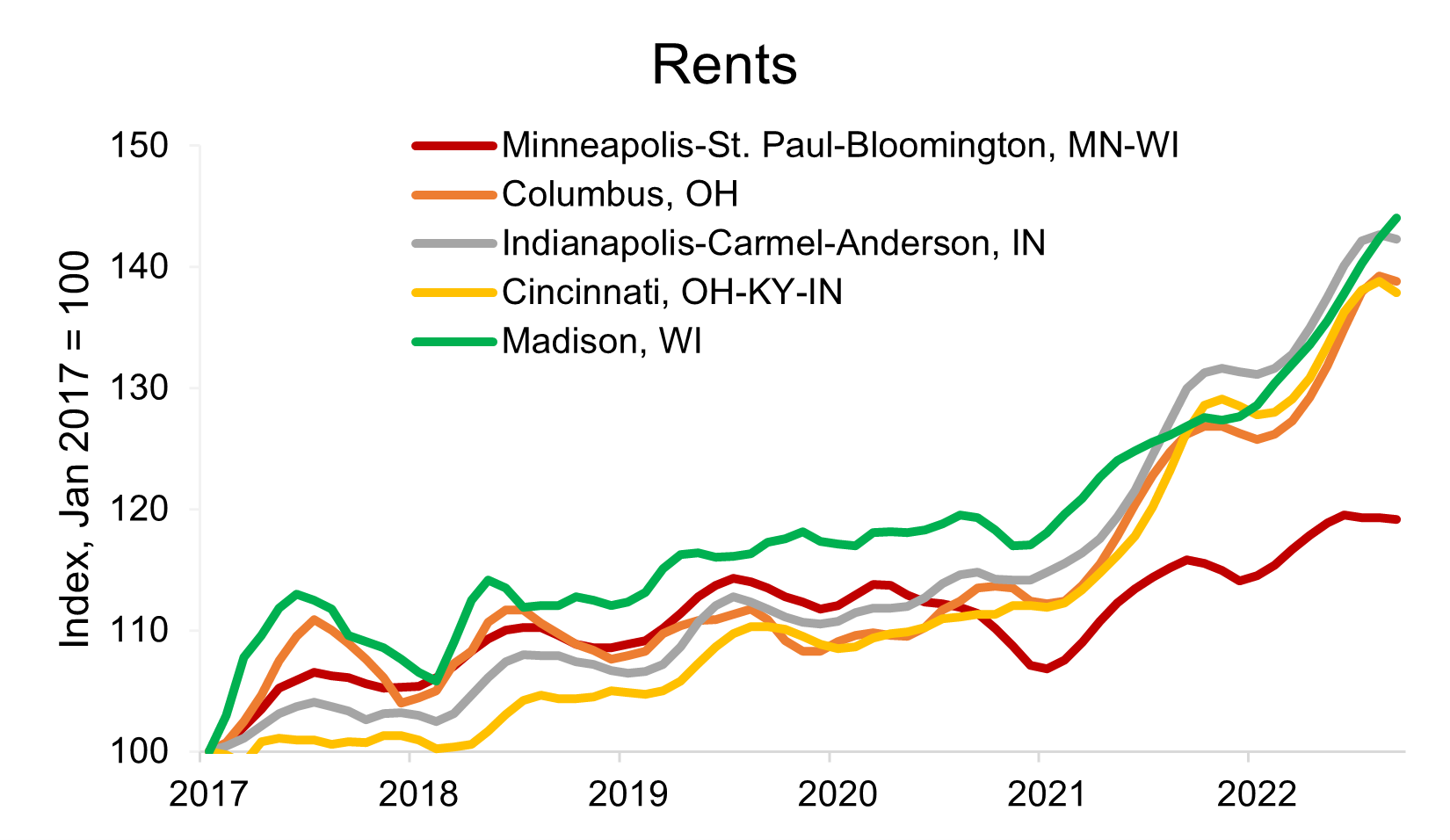

As to the effect of new supply on rents, Minneapolis rents for have grown slower than CPI and the U.S. Average, as well as the neighbouring city of St. Paul. Indeed, despite U.S. rents and inflation growing by around 15 per cent since 2018, rents in Minneapolis have either barely changed or have declined, depending on the type of property observed.

While the story in Minneapolis is more complicated than in Auckland, it still represents an example of how a local area can encourage new supply through cascading reforms. This case study can also highlight that upzoning reforms can be gradually implemented, and a pro-density attitude from governments can induce supply.

Rents

Comparison to other Mid-Western Cities

Minneapolis has reported better housing outcomes than comparable Mid-Western cities over the past few years. The charts below demonstrate that supply has grown faster, rents have barely changed despite an inflationary environment, and homelessness has fallen significantly. While this cannot be causally ascribed to the supply-side reforms, it is more evidence that zoning and supply reforms can help contribute to improved housing outcomes, including for those at the bottom of the housing spectrum.

Some notes on these data

Construction data for 2022 is an estimate of the annualised rate.

Approvals and rental data are for St Paul, Minneapolis, and Bloomington rather than Minneapolis. As these are rate data, and both St Paul and Bloomington have not had supply reform, it is likely that these underestimate the effects of supply reform in Minneapolis (all else equal).

Approvals take time to build, so the effect of supply coming into the market is likely delayed by a year or two.

Rental data is based upon listings, rather than all rents paid. This is likely to be a lagging indicator.

Sources/Read More:

https://www.governing.com/community/how-important-was-the-single-family-housing-ban-in-minneapolis

https://reason.com/2022/05/11/eliminating-single-family-zoning-isnt-the-reason-minneapolis-is-a-yimby-success-story/#:~:text=Minneapolis%2C%20by%20being%20the%20first,an%20explosion%20in%20new%20development.

https://streets.mn/2022/05/06/minneapolis-rents-drop/

https://mobile.twitter.com/janneformpls/status/1523691783758045185